Join WhatsApp Channel

Join WhatsApp Channel

The Indian rupee’s recent trajectory is increasingly emerging as a test case for central bank agility in a fragmented global financial order, with SBI Research warning that the Reserve Bank of India (RBI) now faces a far more complex balancing act than in past currency stress episodes—one that demands precision rather than force.

In its latest Ecowrap report, SBI Research underscores that the nature of external shocks confronting the rupee has fundamentally shifted. Unlike the 2013 taper tantrum, when a singular trigger—US monetary tightening—sparked capital flight, the current phase is defined by overlapping pressures, including geopolitical tensions, energy price volatility and shifting global capital allocations.

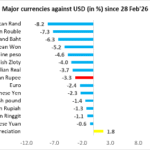

This evolving landscape is already visible in the currency’s performance. The rupee depreciated by 6.4% between April 2025 and late February 2026 even as the dollar index weakened by nearly 6% during the same period—an unusual divergence that signals structural underperformance rather than cyclical weakness. Since then, the currency has weakened further in line with global peers, but the persistence of pressure—reflected in a ₹4.8 decline over 114 days—suggests a slow-burn adjustment driven as much by capital flow dynamics as by macro fundamentals.

What complicates the policy response is that India’s macroeconomic position, by most conventional metrics, remains resilient. Foreign exchange reserves exceeding $700 billion provide import cover of over 10 months, while short-term external debt remains below 20% of reserves and the current account deficit is contained at around 1% of GDP. Yet, as SBI Research cautions, the composition of external liabilities—particularly the still-elevated share of volatile capital flows at 64.5% of reserves—renders the system vulnerable to sudden shifts in investor sentiment.

In effect, the rupee is no longer reacting purely to macroeconomic signals; it is being shaped by the microstructure of currency markets, where liquidity mismatches and regulatory frictions are beginning to amplify volatility. The sharp spike in offshore non-deliverable forward (NDF) premiums—where the one-year premium jumped to 4.19% and the one-month rate doubled in a single day—points to tightening dollar liquidity and growing dislocations between onshore and offshore markets. With outstanding NDF exposures estimated at around $45 billion and banks holding a dominant share, the unwinding of positions amid regulatory constraints risks creating a feedback loop of rising premiums and thinning liquidity.

It is within this increasingly intricate framework that the RBI’s policy challenge is taking shape. The central bank must simultaneously prevent disorderly currency movements, maintain adequate domestic liquidity and preserve growth momentum—objectives that are no longer easily aligned. Intervention in the foreign exchange market, for instance, can stabilize the rupee but may drain rupee liquidity, while easing liquidity conditions could exacerbate depreciation pressures.

SBI Research argues that the solution does not lie in reviving blunt, crisis-era instruments such as large-scale overseas deposit schemes, which had brought in $34 billion during the 2013 episode but are now rendered less effective by higher hedging costs and a decoupling of global yield structures. Instead, the emphasis is shifting towards targeted, market-sensitive interventions—such as carving out a separate dollar window for oil marketing companies, whose daily demand of $250–300 million translates into an annualized $75–80 billion burden on the spot market. By isolating such structural demand, policymakers could improve visibility on genuine market pressures while reducing noise-driven volatility.

Equally critical is the need to recalibrate regulatory measures affecting banks’ foreign exchange positions. The report suggests that imposing limits at the level of trading books rather than entire balance sheets could ease operational constraints and mitigate unintended liquidity tightening, particularly at a time when capital outflows—whether due to portfolio rebalancing or profit booking—are likely to place additional demands on the banking system.

Underlying these recommendations is a broader analytical shift: the notion of the rupee as a passive “shock absorber” is being called into question. While gradual depreciation may help cushion external shocks, SBI Research warns that beyond a certain threshold it risks unanchoring expectations, especially when the magnitude of movement appears disconnected from underlying fundamentals.

Looking ahead, the RBI’s task will be less about defending any specific exchange rate level and more about managing the quality of volatility—ensuring that currency movements remain orderly, liquidity conditions stable and financial markets aligned with broader macroeconomic objectives. In a world where capital flows are increasingly fickle and market signals often distorted, the margin for policy error is narrowing.

The coming months, therefore, are likely to define not just the trajectory of the rupee, but also the contours of India’s evolving monetary and exchange rate framework—one that must rely on calibrated intervention, institutional flexibility and a far deeper engagement with market microstructure than in previous cycles.