Join WhatsApp Channel

Join WhatsApp Channel

Retirement planning is one of the most important pillars of financial well-being, yet many people postpone it until it is almost too late. A successful retirement plan is about ensuring that your money outlasts your life, allowing you to live with dignity, confidence and financial independence. The earlier you begin, the easier it becomes to build a retirement corpus that can withstand inflation, rising healthcare costs and changing lifestyle needs.

Why Start Early?

Time is your greatest financial advantage. Starting early allows investments to benefit from the power of compounding, enabling wealth to grow steadily over decades. It also means you can invest smaller amounts regularly instead of making large contributions later in life. Early planning provides flexibility to adjust your investment strategy as your income, responsibilities and goals evolve, while also offering peace of mind that your future is financially secure.

Factors That Shape Your Retirement Needs

Inflation: Inflation steadily reduces the purchasing power of money. Both economic inflation and lifestyle inflation—the tendency to spend more as income rises—must be factored into retirement planning. Even a 5% annual inflation rate can substantially increase the amount needed after retirement.

Healthcare Costs: Medical expenses typically rise faster than general inflation. As life expectancy increases, planning for healthcare becomes essential to avoid financial strain during retirement.

Lifestyle: Your retirement goals determine how much you need to save. Whether you plan to travel, pursue hobbies or simply maintain your current standard of living, your desired lifestyle will shape your retirement corpus.

Longevity: With advances in healthcare, planning up to age 90 or beyond provides a safety margin and reduces the risk of outliving your savings.

Building a Strong Retirement Corpus

A disciplined investment strategy is the foundation of retirement planning.

Asset allocation plays a critical role. Equities offer higher long-term growth potential and are generally suitable for younger investors with longer investment horizons. Fixed-income instruments such as bonds and fixed deposits provide stability but lower returns, making them more appropriate as retirement approaches. Real estate and alternative investments such as gold or REITs can provide diversification but should complement, not replace, a balanced portfolio.

Liquidity is equally important. Your portfolio should contain sufficient liquid assets to meet short-term expenses without forcing the sale of long-term investments.

Tax planning should also form part of your strategy. Choosing tax-efficient investments and planning withdrawals carefully can improve post-retirement income, particularly as tax laws evolve over time.

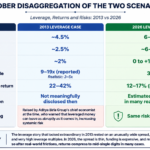

The Cost of Conservative Investing

Consider three investors—aged 35, 45 and 55—planning to retire at 60 with life expectancy assumed at 90 and inflation at 5%.

Across all three cases, a portfolio invested primarily in fixed deposits requires a significantly larger retirement corpus than one with greater equity exposure. For a 35-year-old, the estimated corpus falls from nearly Rs. 5 crore with fixed deposits to about Rs. 3 crore with a predominantly equity portfolio. Similar trends are seen for those aged 45 and 55, demonstrating how long-term growth assets can substantially reduce the savings required to sustain the same retirement lifestyle.

The lesson is not to invest entirely in equities, but to adopt an age-appropriate asset allocation that balances growth with risk.

Common Retirement Planning Mistakes

Some of the most common mistakes include relying solely on provident fund and gratuity, investing only in low-growth assets such as fixed deposits, purchasing insurance products primarily as investments, ignoring inflation and taxation, making premature withdrawals from retirement savings, and simply starting too late. Each of these can significantly reduce the retirement corpus and compromise long-term financial security.

A Secure Retirement Begins Today

Retirement planning is not just about accumulating wealth; it is about creating financial independence for the years when regular income stops. Starting early, maintaining a diversified portfolio, reviewing investments periodically and planning for inflation, healthcare and taxes can make a significant difference to your quality of life after retirement.

Working with a qualified personal finance advisor can help you develop a retirement strategy tailored to your goals, risk profile and income needs. The objective is simple: ensure your money lasts throughout your lifetime so you can enjoy retirement with freedom, dignity and confidence.

Disclaimer: The opinions and views expressed in this article/column are those of the author(s) and do not necessarily reflect the views or positions of South Asian Herald.