Join WhatsApp Channel

Join WhatsApp Channel

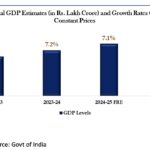

India’s headline growth numbers are racing ahead, but the underlying fiscal arithmetic is tightening in ways that even a robust economy cannot fully obscure. The latest national accounts show real GDP expanding 8.2% in the July–September quarter of FY26, yet the government’s revenue engine is sputtering, the nominal base is unusually weak, and the fiscal roadmap increasingly depends on improvised savings rather than buoyant collections.

The National Statistics Office estimated Q2 real GDP at ₹48.63 trillion ($586 billion), up from ₹44.94 trillion ($541 billion) a year earlier (). Nominal GDP rose 8.7% to ₹85.25 trillion ($1.03 trillion)—barely above real growth—reflecting one of the weakest GDP deflators in recent years. That alone complicates the government’s ability to meet its 4.4% fiscal deficit target, which was framed on an assumed 10.1% nominal growth.

The fiscal deficit is rising even as revenue deficit narrows

Aditi Nayar, Chief Economist at ICRA Ltd, said the Centre’s fiscal deficit widened to ₹8.3 trillion ($100 billion) during April–October FY26, about 53% of the full-year target, compared with ₹7.5 trillion ($90 billion) (48% of last year’s provisional estimate) in the same period of FY25.

The gap is being driven almost entirely by a front-loaded push in capital spending, which surged 32% year-on-year to ₹6.2 trillion ($75 billion) in the first seven months. Revenue spending stayed flat, helping compress the revenue deficit to ₹2.4 trillion ($29 billion) from ₹3 trillion ($36 billion) a year earlier.

But the numbers flatter to deceive. Non-tax revenues soared 22%, thanks largely to the Reserve Bank of India’s oversized surplus transfer, while net tax revenues actually contracted 2% because of higher transfers to states.

Tax math turns harsh as shortfalls deepen

The tax picture is where the fiscal strain sharpens. Gross tax revenues grew just 4% in April–October—hopelessly out of sync with the 22% year-on-year surge required from November to March to meet the Budget target of ₹42.7 trillion ($515 billion).

October’s 14% jump came off a low base. Personal income tax collections rose 6.9%, corporate tax 5.2%, and indirect taxes crawled at 2.6%, with customs duty actually contracting 2.5%.

“Central GST would need to grow almost 18% in the last five months—an unrealistic ask,” Nayar warned. ICRA expects a ₹1.2–1.5 trillion ($14–18 billion) tax shortfall, partially offset by roughly ₹500 billion ($6 billion) in additional non-tax revenue.

The outcome: New Delhi is likely to rely on expenditure savings and quiet underspending across ministries to prevent the deficit from slipping, a familiar tactic in years when revenue disappoints.

Strong headline numbers cannot hide the nominal drag

Economists point out that India’s enviable real growth masks an uncomfortable reality: nominal growth—key for tax buoyancy—remains muted. That divergence has been driven by an “unusually low” GDP deflator, with wholesale inflation barely above zero.

Madan Sabnavis, Chief Economist at Bank of Baroda, said the 8.2% print lifts first-half growth to 8%, but “nominal GDP growth of just half a percentage point above real growth means the fiscal deficit ratio becomes harder to meet.”

Still, Sabnavis noted that the underlying sectoral performance is encouraging. Agriculture grew 3.5%, manufacturing 9.1%, construction 7.4%, and services were led by financial and real-estate activity at 10.2%. Tourism-linked categories accelerated to 7.4%, and public administration logged 9.7% (). Corporate results corroborated the manufacturing strength, while strong cement and steel consumption underpinned construction.

Exports were a bright spot, rising 11% in Q2, but Sabnavis cautioned that the impact of punitive US tariffs “will get starker in October–November,” even if the GST cuts may soften the blow.

External headwinds are real, but domestic demand stays firm

Shivaan Tandon, Asia Economist at Capital Economics, said the Q3 calendar-year GDP figure (India’s Q2 fiscal quarter) “was well above expectations,” aided partly by the weak deflator but underpinned by genuine strength.

He warned, however, that sustaining this pace is difficult: “US tariffs will weigh more visibly in Q4 than Q3. But consumption—helped by GST cuts, low inflation and easier monetary conditions—should stay resilient.” Tandon now expects 7.5% growth in 2025 and 6.5% in 2026, keeping India at the top of the global growth league.

Even with strong growth, policy room remains constrained

Upasna Bhardwaj, Chief Economist at Kotak Mahindra Bank, said the upside surprise “comes on the back of a very low deflator,” and that nominal softness “signals tepid underlying activity.” She expects a 25-basis-point rate cut, underscoring that inflation is benign and real activity, while strong, is not overheating.

A high-growth economy boxed in by its own numbers

India’s macro story in FY26 is becoming paradoxical. Output growth is broad-based and impressive. Manufacturing is humming, construction is resilient, and services are powering ahead. Yet the fiscal framework remains delicately balanced on weak nominal growth, underperforming taxes, and the need for sharp expenditure restraint in the final stretch of the year.

The government’s ability to meet its fiscal deficit target will hinge not on growth—where India continues to outperform—but on whether the final months deliver a tax surge that so far shows no sign of materializing. Non-tax revenues and administrative savings can only plug part of the hole.

India ends the quarter looking strong, but the numbers beneath the surface tell a more complicated, less comfortable story—one where the economy may be sprinting, but the fiscal engine is struggling to keep up.