Join WhatsApp Channel

Join WhatsApp Channel

India’s rupee sliding close to ₹90 per U.S. dollar has revived the argument that currency depreciation should boost export competitiveness. But trade data and new analysis from the Global Trade Research Initiative (GTRI) show that the rupee’s fall has had little impact because India’s export ecosystem is too costly and over-regulated for exchange-rate gains to matter.

The long-term trend tells the story clearly. In 2013, the rupee traded near ₹60, and India’s merchandise exports stood at $313 billion. Today, after nearly 50 per cent depreciation, exports have risen only to about $440 billion. A weaker currency should have given exporters a sharp advantage, yet the growth has been marginal. GTRI says India’s export stagnation has less to do with the rupee’s value and more to do with what it calls a “high-cost, friction-heavy manufacturing environment.”

GTRI notes several bottlenecks that blunt any benefit from depreciation:

- High input tariffs that raise the cost of imported intermediates.

- Quality Control Orders (QCOs) that have slowed supply chains and restricted access to critical components.

- Costly logistics, far above those in competing export economies.

- Heavy reliance on imported intermediates and capital goods, which immediately become more expensive when the rupee weakens.

These frictions, GTRI says, have turned India into a system where “a falling rupee does not translate into rising exports.”

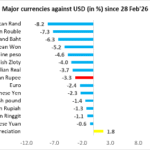

The current phase of depreciation reflects global and domestic pressures. A stronger U.S. dollar, driven by elevated Federal Reserve rates, has weakened most Asian currencies this year. India has also seen $16.4 billion in foreign portfolio outflows from equities in 2025, adding pressure on the rupee. A wider trade deficit — fueled partly by rising gold imports — and uncertainty around U.S. tariff decisions have further dented sentiment.

Even as the rupee weakens nominally, it remains overvalued in real terms. The Real Effective Exchange Rate (REER) is at 108.14, signaling an estimated 8 per cent overvaluation once inflation differences are factored in. This contradiction underscores GTRI’s central point: India’s production costs and regulatory burden keep exports expensive even when the currency appears competitive.

Exporters say the depreciation benefit is often offset immediately. Imported inputs cost more, financing becomes costlier, and regulatory delays add to expenses. For sectors such as electronics, petroleum products, machinery, chemicals and auto components — all heavily import-dependent — a weaker rupee intensifies pressure rather than offering relief. Only a few segments, such as IT services and pharmaceuticals, stand to gain meaningfully.

The Reserve Bank of India (RBI) intervened last week after the rupee breached ₹88.80, triggering the sharpest single-day fall in more than three years. The RBI sold dollars in the spot and non-deliverable forward markets to rein in volatility. Officials maintain that reserves remain comfortable and the currency’s moves reflect normal dollar demand. Market forecasts, however, indicate further depreciation, with many desks expecting the rupee to breach ₹90, and some projecting up to 5% depreciation in CY25.

Higher imported inflation from the weaker rupee could also limit the space for interest-rate cuts, adding another layer of strain for manufacturers relying on working-capital credit.

Despite the pressures, GTRI sees signs of gradual course correction. The government’s recent rollback of several QCOs — especially those affecting industrial inputs — suggests recognition of supply-chain disruptions. GST rate rationalization efforts may ease compliance and lower input costs for exporters, while long-pending labor reforms have the potential to reduce operational rigidity and improve scale.

But GTRI stresses that these steps need to be deeper, faster and more coherent. Without a sustained reduction in tariffs, regulatory density and logistics inefficiencies, India’s exporters will remain unable to leverage a competitive exchange rate. The rupee’s slide may draw political attention, but GTRI says the real challenge is structural: unless domestic cost pressures are addressed, depreciation will continue to be a cosmetic change with limited trade impact.

For now, the rupee nearing 90 has exposed a fundamental reality — India’s export competitiveness depends far more on internal reforms than on currency movements. The country’s export engine, GTRI warns, cannot accelerate unless the underlying cost structure is reworked to allow a weaker rupee to finally matter.

Related posts:

Volatile Capital Flows Put RBI in Policy Crosshairs as Rupee Weakens

Volatile Capital Flows Put RBI in Policy Crosshairs as Rupee Weakens

Beyond Oil: How the West Asia Conflict Is Rewiring India’s Economic Stability

Beyond Oil: How the West Asia Conflict Is Rewiring India’s Economic Stability

Trade Potential vs Banking Reality: India’s Russia Strategy Hits Settlement Wall

Trade Potential vs Banking Reality: India’s Russia Strategy Hits Settlement Wall

Iran War Raises Energy, Trade and Inflation Risks for India and South Asia

Iran War Raises Energy, Trade and Inflation Risks for India and South Asia