Join WhatsApp Channel

Join WhatsApp Channel

The escalating conflict in West Asia is rapidly emerging as a multi-dimensional economic shock for India, threatening to unsettle currency stability, capital flows, and macroeconomic balances, even as policymakers rely on domestic demand and foreign exchange buffers to cushion the fallout.

A detailed assessment by State Bank of India’s research team underscores that the crisis—centered around disruptions in key energy supply routes such as the Strait of Hormuz—has already triggered one of the largest global oil supply shocks in recent history, with an estimated disruption of nearly 8 million barrels per day in March alone.

The resulting volatility, the report warns, is not merely cyclical but potentially structural, raising the specter of stagflation globally and complicating monetary policy responses, particularly in advanced economies.

Oil shock and macro vulnerability

India, which imports over 85% of its crude oil needs, finds itself acutely exposed. The Indian crude basket, already elevated at around $119 per barrel in March, could rise to $125–$137 if hostilities persist, significantly inflating the country’s import bill.

The transmission is immediate and unforgiving: every $1 increase in crude prices could add $1.5–2 billion to India’s annual import bill, widening the current account deficit (CAD), which is now projected at 1.3–1.5% of GDP (roughly $60 billion) for FY27.

This comes against the backdrop of an already fragile global environment marked by trade disruptions, tariff frictions, and weakening demand in major economies.

Rupee under pressure, limits of depreciation

The Indian rupee has emerged as an early casualty. Having breached the 93-per-dollar mark for the first time, the currency has depreciated sharply within weeks of the conflict’s escalation.

While the Reserve Bank of India has intervened aggressively—selling an estimated $53 billion between April and December 2025—the report suggests that the traditional argument of currency depreciation acting as a “shock absorber” is weakening.

Empirical analysis shows export responsiveness to exchange rate movements has become statistically insignificant in the current environment, implying that a weaker rupee may not meaningfully boost exports.

In a prolonged conflict scenario, the rupee could slide further towards 96 per dollar, raising imported inflation risks without delivering commensurate export gains.

Capital flight and investment stress

External sector pressures are being compounded by sharp capital outflows. Foreign institutional investors (FIIs) have pulled out approximately $14.3 billion in FY26 so far, with March alone witnessing outflows nearing $11.8 billion—potentially the highest monthly exodus since the 1991 balance-of-payments crisis.

Simultaneously, India’s net foreign direct investment (FDI) has turned negative for five consecutive months, as repatriation and outward investments outpace fresh inflows.

This dual drain—portfolio and direct investment—has placed additional strain on the balance of payments, which is expected to remain in deficit for the third straight year at around $24–25 billion.

Sectoral stress and corporate impact

The ripple effects are spreading across corporate India. Sectors accounting for nearly 40% of listed company revenues—including fertilizers, metals, logistics, aviation, and construction—face margin compression due to higher input costs and supply disruptions.

In a severe scenario, revenue losses could amount to as much as 0.8% of GDP, underscoring the scale of the shock.

Bond markets have already reacted, with the 10-year government security yield rising to 6.84%, signaling tighter financial conditions ahead.

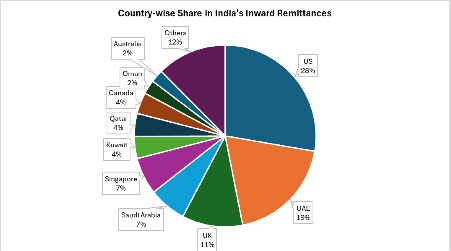

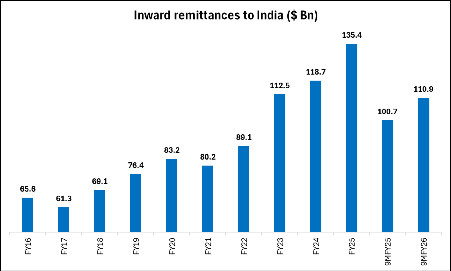

Remittances: a rare cushion

One area of relative resilience is remittances. India, the world’s largest recipient of overseas remittances, is expected to receive $140–145 billion in FY26, supported by its vast diaspora, particularly in the Gulf region.

However, even this buffer is not immune. A prolonged conflict could disrupt employment in construction and energy sectors in West Asia, potentially triggering reverse migration and dampening inflows in the medium term.

Agriculture and inflation risks

While agricultural production remains largely insulated for now, the report flags rising risks of input-cost inflation—particularly in fertilizers, diesel, and logistics—which could feed into food prices over the next crop cycles.

This delayed transmission could complicate inflation management, especially if energy prices remain elevated.

Policy buffers and strategic response

Despite the mounting pressures, India retains some macroeconomic buffers. Foreign exchange reserves, supplemented by a $75 billion bilateral swap arrangement with Japan, provide a degree of insulation against external shocks.

The government has also announced targeted interventions, including a $6 billion economic stabilization fund and export support measures to mitigate logistics disruptions.

Crucially, the report emphasizes that India’s best defense lies in sustaining domestic demand, diversifying export markets, and accelerating import substitution through technological and efficiency gains.

A fragile equilibrium

Yet, the broader assessment is sobering. The crisis, analysts suggest, is unfolding with “second and third-order effects” that could reshape global energy markets and capital flows in more durable ways.

For India, the challenge is no longer limited to managing a temporary external shock. It is about navigating a more volatile global order where traditional policy levers—currency depreciation, capital inflows, and benign commodity cycles—can no longer be taken for granted.

In that sense, the West Asia conflict may prove less a transient disruption and more a stress test of India’s evolving economic resilience.

Related posts:

Oil, Inflation and the Rupee: The Economic Fallout of the West Asia Conflict

Oil, Inflation and the Rupee: The Economic Fallout of the West Asia Conflict

Rupee Near 90 Fails to Lift Exports; GTRI Flags Structural Barriers as the Real Drag

Rupee Near 90 Fails to Lift Exports; GTRI Flags Structural Barriers as the Real Drag

Iran War Raises Energy, Trade and Inflation Risks for India and South Asia

Iran War Raises Energy, Trade and Inflation Risks for India and South Asia

Modi Flags Economic Fallout as West Asia Conflict Disrupts Supply Chains

Modi Flags Economic Fallout as West Asia Conflict Disrupts Supply Chains