Join WhatsApp Channel

Join WhatsApp Channel

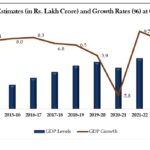

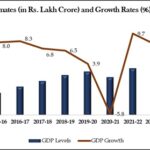

India’s economy expanded by 7.6% in fiscal year 2026, according to the Second Advance Estimates released under a newly rebased national accounts series. In a global environment where the US, Europe and China are all struggling to generate growth above 2–3%, the number stands out. For global investors and policymakers, it reinforces India’s reputation as the world’s fastest-growing major economy.

A closer look at the data, however, shows that the headline figure conceals significant structural imbalances. Growth is increasingly concentrated in manufacturing and select services, while agriculture, construction and rural incomes — sectors that employ the majority of India’s workforce — continue to lag. The result is an economy that is expanding rapidly in aggregate, but unevenly beneath the surface.

A new GDP series, a different growth mix

The estimates were released by the Ministry of Statistics and Programme Implementation through the National Statistical Office, using 2022–23 as the new base year, replacing the earlier 2011–12 series. The rebasing has materially altered the composition of growth.

Under the new series, gross fixed capital formation (investment) is estimated at 31.7% of GDP, among the highest levels seen since the mid-2000s investment boom. By contrast, private consumption now accounts for 56.7% of GDP, down from around 58–60% under the previous base.

In dollar terms, this shift is substantial. In a roughly $3.5 trillion economy, a one-percentage-point change in the consumption share represents demand of more than $40 billion. The revised data suggest that India’s growth is now more investment-driven and less consumption-led than previously assumed — a configuration that tends to be more sensitive to policy changes, financing conditions and external shocks.

Another notable feature is that gross value added (GVA) has grown slightly faster than GDP for two consecutive years. In FY26, GVA rose 7.7%, marginally above GDP growth of 7.6%, implying a negative contribution from net indirect taxes. This indicates that tax revenues have not kept pace with output growth, despite nominal GDP expanding by about 8.6%, raising questions about fiscal buoyancy.

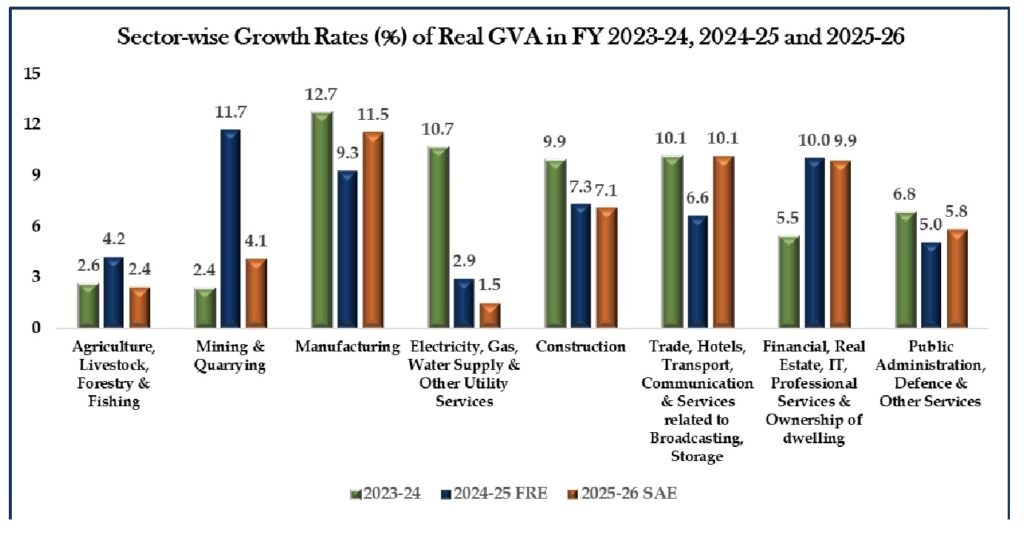

Manufacturing powers ahead

Manufacturing has emerged as the dominant growth engine. The sector expanded by 11.5% in real terms in FY26, contributing the largest share to incremental output. Over the past three years, manufacturing GVA has grown at an average rate of roughly 11%, far outpacing the overall economy.

Madan Sabnavis, Chief Economist at Bank of Baroda, said the strength of manufacturing has been the biggest surprise in the data. “Manufacturing has spearheaded overall GDP growth with 11.5% growth, and manufacturing GVA has recorded consistently high growth of around 11% over the last three years,” he said.

Yet manufacturing still employs less than one-fifth of India’s workforce, and the capital intensity of growth has increased. Much of the expansion has been driven by large firms benefiting from public infrastructure spending, corporate balance-sheet repair and production-linked incentives. Credit growth to small and medium manufacturers has been far more modest, limiting job creation and spillovers into mass consumption.

Construction slows, jobs feel the strain

Construction — one of India’s most labor-intensive sectors — grew by 7.1% in FY26, slower than in the immediate post-pandemic years. The sector employs more than 13% of the workforce, making it critical for income generation among migrant and informal workers.

Economists link the slowdown partly to a shift in housing demand toward mid-range and premium segments, while affordable housing — which generates more employment — has weakened. The result is a disconnect between GDP growth and job creation, contributing to subdued consumption growth despite strong headline numbers.

Agriculture remains the weakest link

The most persistent drag on the economy continues to be agriculture. The sector grew just 2.4% in FY26, less than one-third of overall GDP growth and far below manufacturing’s pace. In the third quarter — traditionally a strong period due to festival-related demand — agricultural growth slowed to about 1.4%, even as GDP expanded 7.8%.

With over 40% of India’s workforce dependent on agriculture, such weak growth has outsized consequences. After adjusting for population growth, real per-worker income growth in agriculture is estimated at just 1–1.5%, insufficient to support a broad-based consumption recovery.

“Agriculture growth is lower based on the new series, but it could improve once final rabi crop numbers are available,” Sabnavis noted. For now, however, rural demand continues to trail urban consumption, which is being driven largely by salaried households.

Services provide stability — with caveats

Services grew a robust 9% in FY26, helping stabilize overall growth. Trade, transport, hospitality and communications expanded at double-digit rates, while finance, real estate and professional services also grew close to 10%.

However, public administration and defense spending slowed, reflecting weaker state-level expenditure. Aditi Nayar, Chief Economist at ICRA, said this moderation weighed on non-manufacturing sectors such as mining, electricity and construction, even as manufacturing and services remained resilient.

Big-picture implications

India’s economy has now recorded three consecutive years of growth above 7%, an achievement unmatched by any other large economy. Shilan Shah, Deputy Chief Emerging Markets Economist at Capital Economics, said the new data confirm that “the economy is performing strongly,” even though the rebasing shows the nominal size of the economy is somewhat smaller than previously estimated.

For global investors, the message is nuanced. India’s growth momentum remains strong, supported by manufacturing, services and public investment. But the data also highlight structural risks: weak farm incomes, slowing job creation in labor-intensive sectors, and a growth model increasingly reliant on capital rather than consumption.

Forecasts for FY27 cluster around 7–7.5% growth. Achieving that will require manufacturing and services to sustain their current pace — and, crucially, a pickup in agriculture and construction. Without that, India’s expansion may remain impressive on paper, but narrower than the headline numbers suggest.