Join WhatsApp Channel

Join WhatsApp Channel

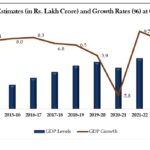

India’s economic growth is projected to moderate to 6.6 per cent in FY27, as rising energy prices linked to the Middle East conflict and ongoing supply chain disruptions weigh on activity, the World Bank said in its latest India Development Update released on Thursday.

Despite the expected slowdown, India will continue to rank among the world’s fastest-growing major economies, supported by strong macroeconomic fundamentals and policy buffers, the report noted.

The multilateral lender flagged “significant downside risks” from geopolitical tensions but said India’s substantial foreign exchange reserves, low inflation, predominantly rupee-denominated public debt and a stable financial sector provide resilience against external shocks. Efforts to diversify trade have also helped cushion the impact of global volatility.

“Boosting private sector-led growth will be critical to strengthening economic resilience and supporting more young people to enter the workforce,” said World Bank Acting Director for India, Paul Procee. He added that a predictable, business-friendly policy environment would be key to unlocking investments and generating jobs across sectors such as energy, infrastructure, manufacturing, tourism, healthcare and agribusiness.

The India Development Update accompanies the World Bank Group’s broader South Asia Economic Update, which projects regional growth to slow to 6.3 per cent in 2026 from 7 per cent in 2025, largely due to disruptions in global energy markets. Growth in the region is expected to recover to 6.9 per cent in 2027, maintaining its position as the fastest-growing among emerging market and developing economies.

The regional report also examined the increasing use of industrial policy across South Asia, noting that governments in the region deploy such measures at nearly twice the rate seen in other emerging economies, albeit with mixed outcomes.

“South Asia’s mixed success on industrial policy in part reflects the region’s limited implementation capacity, fiscal space, and market size in some countries,” said World Bank Group Chief Economist for South Asia, Franziska Ohnsorge.

The report suggested that while broad-based structural reforms should remain the priority, targeted and well-designed industrial policies could help address specific market failures. These include measures such as developing industrial parks, expanding skill development programmes, improving market access and enhancing export quality standards.

It further recommended a calibrated policy push in sectors such as urban development, tourism and digital services, alongside improvements in regulatory predictability and state capacity—seen as critical to sustaining growth and boosting job creation across the region.

Related posts:

Global Growth Outlook Darkens, But South Asia Defies Gloom with Strong Momentum

Global Growth Outlook Darkens, But South Asia Defies Gloom with Strong Momentum

Weaponizing Remittances: How the US is Threatening South Asia’s Stability

Weaponizing Remittances: How the US is Threatening South Asia’s Stability

Despite Losing Steam, India’s Economy Holds Its Lead Over China’s

Despite Losing Steam, India’s Economy Holds Its Lead Over China’s

South Asia’s Recovery Uneven as India Holds Firm, Pakistan and Sri Lanka Struggle

South Asia’s Recovery Uneven as India Holds Firm, Pakistan and Sri Lanka Struggle